Electric car market statistics

Published May 15, 2026

- The two millionth BEV was registered in the UK in April 2026, marking a significant milestone for electrification.

- Used BEV sales rose 32.0% YoY in Q1 2026, with almost 87,000 changing hands. EVs accounted for one in 23 used cars sold in the period.

- The SMMT revised its full-year 2026 BEV market share forecast from 28.5% to 26.8% in its April 2026 outlook, citing softer-than-expected Q1 demand.

Our EV market statistics guide brings together the latest UK registration data, powertrain trends, and expert commentary, covering the developments that matter to journalists, industry professionals, and car buyers alike.

For broader new and used car market data, see our UK car market statistics guide.

Get a free valuation

The current state of the new EV market

- New car registrations reached 149,247 in April 2026, a 24.0% YoY increase, which marked the strongest April since 2019.

- BEVs led the recovery, rising 59.1% to 39,084 units and a 26.2% market share.

- Both figures partly reflect the low base set in April 2025, when buyers brought forward purchases ahead of VED changes and the Expensive Car Supplement (ECS) being extended to BEVs for the first time.

April 2026 vs April 2025 - registrations by powertrain

| Powertrain | Apr 2026 | Apr 2025 | % change | Share Apr 2026 | Share Apr 2025 |

|---|---|---|---|---|---|

| BEV | 39,084 | 24,558 | +59.1% | 26.2% | 20.4% |

| HEV | 19,711 | 16,586 | +18.8% | 13.2% | 13.8% |

| PHEV | 20,597 | 14,073 | +46.4% | 13.8% | 11.7% |

| Petrol | 63,541 | 58,733 | +8.2% | 42.6% | 48.8% |

| Diesel | 6,314 | 6,381 | -1.0% | 4.2% | 5.3% |

| Total | 149,247 | 120,331 | +24.0% |

Please note: In SMMT reporting, MHEV registrations are included within the petrol and diesel figures.

Source: SMMT

Key takeaways - April 2026

- BEVs rose 59.1% to 39,084 units, claiming a 26.2% market share.

- PHEVs grew 46.4% to 20,597 units, reaching a 13.8% market share - and HEVs increased by 18.8% to 19,711, achieving a 13.2% share.

- Electrified vehicles combined (BEVs, PHEVs, and HEVs) accounted for 53.2% of all registrations, outnumbering ICE transactions.

- Petrol's market share contracted from 48.8% to 42.6% YoY, although volume grew by 8.2%.

- Diesel accounted for 4.2% of the market, down from 5.3% in April 2025.

- The SMMT's YTD BEV share of 23.1% at the end of April is almost ten percentage points below the ZEV Mandate's 33% target for 2026.

webuyanycar's head of technical services, Richard Evans said:

“The two millionth BEV registration is a clear marker of how far the UK's electric car market has grown over the past two decades. Volume has increased substantially year on year, and the range of available models continues to broaden, giving more buyers a viable electric option at a wider range of price points.”

“PHEV demand has also been a consistent feature of the market in early 2026, with growth of 46.4% in April pointing to a strong appetite for plug-in hybrids across both fleet and private channels. Buyers appear to be adopting electrification at a pace that suits their own circumstances, and PHEVs are playing a significant role in that transition.”

EV market trends: January to April 2025 vs 2026

YTD registrations by powertrain - January to April 2025 vs 2026

| Powertrain | YTD 2026 | YTD 2025 | % change | Share 2026 | Share 2025 |

|---|---|---|---|---|---|

| BEV | 176,698 | 144,749 | +22.1% | 23.1% | 20.7% |

| HEV | 111,083 | 102,591 | +8.3% | 14.5% | 14.6% |

| PHEV | 99,263 | 67,759 | +46.5% | 13.0% | 9.7% |

| Petrol | 340,230 | 345,520 | -1.5% | 44.5% | 49.3% |

| Diesel | 36,827 | 40,214 | -8.4% | 4.8% | 5.7% |

| Total | 764,101 | 700,833 | +9.05% |

Key YTD takeaways

- BEVs grew their YTD market share from 20.7% to 23.1%, a gain of 2.4% with volume up 22.1% to 176,698 units.

- PHEVs recorded the strongest YTD growth at +46.5%, reaching 99,263 registrations compared with 67,759 in the same period in 2025.

- Petrol registrations fell 1.5% YoY, with market share contracting from 49.3% to 44.5%.

- Diesel fell 8.4% YoY, accounting for 4.8% of the market compared with 5.7% in the same period in 2025.

- Total market volume grew 9.05% YTD to 764,101 registrations.

Key EV market developments Q1/Q2 2026

Electric Car Grant: Expansion and updates

The UK Government's Electric Car Grant (ECG) scheme, launched in July 2025, offers point-of-sale discounts of up to £3,750 on eligible new electric cars. As of May 2026, more than 50 models qualify. Refer to the official GOV.UK page for the full confirmed list.

For a full breakdown of the scheme and how it works, see our Electric Car Grant guide.

ZEV Mandate: 2026 progress

The ZEV Mandate sets annual targets for zero-emission vehicle sales as a proportion of each manufacturer's total registrations. The target for 2026 is 33%.

- BEVs held a 23.1% market share YTD through April 2026, almost 10% below the 33% mandate target.

- The SMMT's revised full-year 2026 BEV forecast of 26.8% represents strong growth on 2025's 23.4%, though it falls short of the mandate level. The revision reflects a subdued start to 2026 rather than a reversal of the longer-term trend.

- The SMMT's April 2026 outlook notes that rising petrol prices could support BEV demand, while higher energy costs, the planned introduction of a per-mile electricity charge for EVs from 2028 (eVED), and borrowing costs represent potential headwinds.

- In its May 2026 commentary, the SMMT called for a review of the ZEV Mandate transition timeline. Chief Executive Mike Hawes said: "The mounting cost of compliance threatens to limit consumer choice, overall decarbonisation and the sector's competitiveness."

New car market share by powertrain (2018-2027)

The table below tracks the powertrain composition of UK new car registrations from 2018 to 2025. Forecast figures for 2026 and 2027 are drawn from the SMMT's April 2026 New Car and Van Outlook.

| Year | BEV | HEV | PHEV | Petrol | Diesel |

|---|---|---|---|---|---|

| 2027 (forecast) | 32.0% | 15.4% | 14.8% | 34.4% | 3.4% |

| 2026 (forecast) | 26.8% | 14.8% | 13.5% | 40.6% | 4.3% |

| 2025 | 23.4% | 13.9% | 11.1% | 46.4% | 5.1% |

| 2024 | 19.6% | 13.4% | 8.6% | 52.2% | 6.3% |

| 2023 | 16.5% | 12.6% | 7.4% | 56.0% | 7.5% |

| 2022 | 16.6% | 11.6% | 6.3% | 55.9% | 9.6% |

| 2021 | 11.6% | 8.9% | 7.0% | 58.3% | 14.2% |

| 2020 | 6.6% | 6.7% | 4.1% | 62.7% | 19.8% |

| 2019 | 1.6% | 4.2% | 1.5% | 66.0% | 26.6% |

| 2018 | 0.7% | 3.4% | 1.9% | 62.3% | 31.7% |

Source: SMMT.

SMMT's new car outlook explained

2026 outlook

- The SMMT's April 2026 outlook projects total new car registrations of 2.093 million units for the full year, around a 3.6% increase on 2025's total of 2.021 million, and an upgrade from the January 2026 forecast of 2.048 million.

- BEVs are forecast to reach a 26.8% market share, up from 23.4% in 2025. The forecast was revised down from 28.5% in the January 2026 outlook following weaker than expected Q1 demand.

- PHEVs are projected to reach a 13.5% market share (up from 11.1% in 2025).

- HEVs are expected to reach a 14.8% market share.

- Petrol market share is projected to fall to 40.6% from 46.4% in 2025.

- Diesel market share is forecast to fall to 4.3% from 5.1% in 2025.

2027 outlook

- The SMMT forecasts 2.121 million new car registrations in 2027, a 1.4% increase on the 2026 projected figure.

- BEVs are projected to grow 21.0% in volume terms, reaching a 32.0% market share, compared with the ZEV Mandate's 38% target for 2027.

- PHEVs are forecast to grow 10.4%, driving market share up to 14.8%.

- HEVs are expected to grow 5.3%, raising market share to 15.4%.

- Petrol registrations are projected to fall 14.1%, reducing market share to 34.4%.

- Diesel registrations are forecast to decline 18.3%, cutting market share to 3.4%.

webuyanycar's head of technical services, Richard Evans said:

“The SMMT's April 2026 outlook shows a market in which overall volume is growing but the powertrain mix continues to shift. The upward revision to total registrations, alongside the slight adjustment of projected BEV share, reflects a market where buyers are returning in number but choosing across a wider range of powertrain options than forecasters had earlier anticipated.”

“For buyers considering an EV purchase in 2026, the Electric Car Grant covers an expanding range of models and the secondhand market is growing in both volume and variety. Used BEV sales grew 32.0% in Q1 2026 relative to the same period in 2025, offering an increasing number of options for buyers who prefer not to purchase new.”

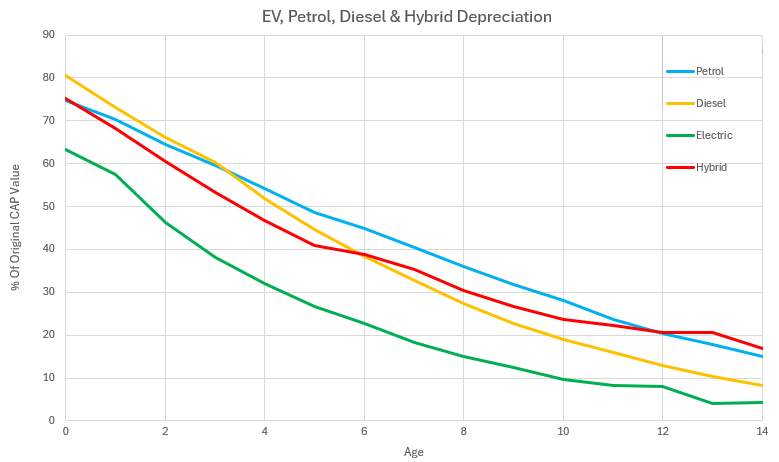

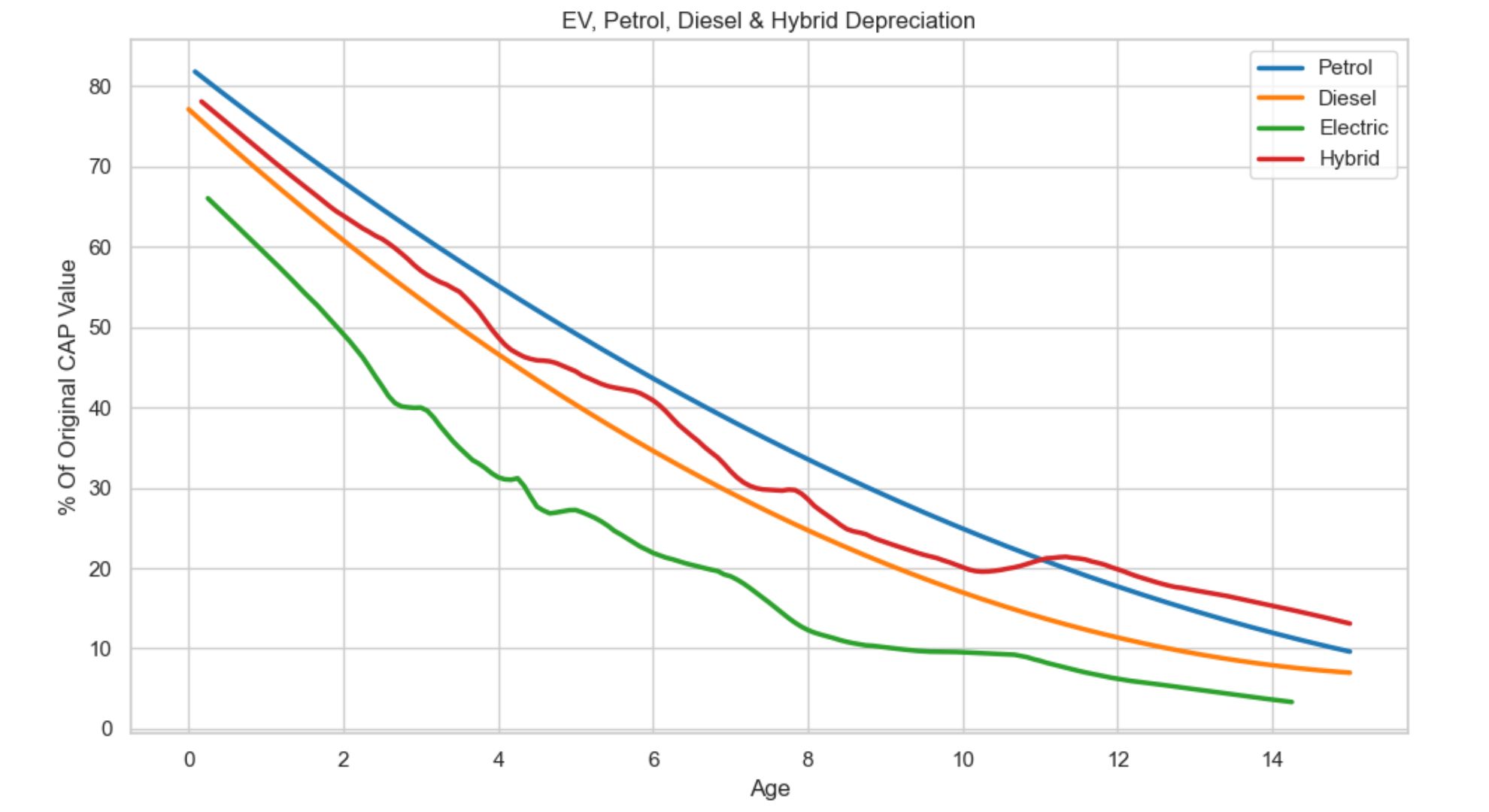

Resale value of used EVs

In May 2026, webuyanycar published updated data on average depreciation rates across powertrain types. The chart below compares the average EV's depreciation against petrol, diesel, and hybrid vehicles, and shows how the picture has changed since the previous dataset was published in August 2025.

May 2026

August 2025

Key findings

- On average, EVs lose approximately 36% of their value at year zero and around 54% after two years. Our August 2025 data showed losses of approximately 34% and 50% at those same intervals.

- The average EV retained approximately 32% of its brand-new value at four years in the May 2026 data, compared with around 28% in the August 2025 data.

- Petrol cars show strong values across the full 15-year curve, retaining around 75% at year zero and approximately 15% at year 14.

- Diesel residuals in the zero-to-three-year range are stronger in May 2026 than in August 2025, sitting above petrol at around 81% in year zero – at around 60% in year three.

- Petrol eventually takes the lead around year four.

- Hybrids take second place from around year six – and finally overtake petrol at year 12.

- EVs depreciate faster than all other powertrain types across the full 15-year curve. The gap narrows slightly from around year eight onward.

- EVs with strong brand reputations, higher performance specifications, and longer ranges may hold their value above the segment average.

webuyanycar's head of technical services, Richard Evans said:

“Our latest depreciation data shows that EVs continue to lose value faster than petrol, diesel, and hybrid cars across the full ownership lifecycle. At four years, the average EV retains around 32% of its original value, compared with 28% in our August 2025 data, a modest but directionally positive shift.”

“The used EV market is still maturing relative to petrol and diesel, where residual value patterns are well established across decades of data. As used EV supply grows, buyer familiarity increases, and the model range broadens, residual values may continue to improve.”

“Whether that trend continues will depend on a number of factors, including the pace of new model introductions and how quickly consumers become comfortable with older battery technology.”

How has the UK's new EV market share grown over time?

BEV registrations have grown significantly over the past decade, rising from a small fraction of the market to become one of the most common powertrain choices in new car sales.

- In 2016, BEVs accounted for 1.4% of all new vehicle registrations.

- In 2025, BEVs reached a 23.4% market share, with PHEVs adding a further 11.1%, bringing the total plug-in share to 34.5%.

- Annual BEV registrations grew from 36,907 in 2016 to approximately 473,000 in 2025.

- The SMMT's April 2026 forecast projects a 26.8% BEV market share for 2026, revised down from the January 2026 projection of 28.5%.

- At the forecast volume of approximately 562,000 BEV registrations, this would represent over 15 times the 2016 total.

How many BEVs are there in the UK?

The two millionth BEV was registered in the UK in April 2026, bringing the cumulative total to 2,012,758 at the end of the month.

As of the end of April 2026, BEVs made up approximately 5.7% of the UK's 34.49 million car parc.

EV chargepoint availability report (Zapmap)

EV chargepoint growth trends 2020 to 2026

Between January 2020 and January 2026, the number of public EV charging devices in the UK grew from 16,505 to 88,513, an increase of 436%.

At the end of April 2026, there were 120,388 EV chargers across 46,333 locations in the UK. In April alone, 1,308 net new EV chargers were added.

Public charger speeds

In February 2026, Zapmap and the Department for Transport updated their power band naming conventions:

- Standard (3kW to 7.9kW) and Standard Plus (8kW to 49kW) replaced the previous Slow and Fast categories.

- Rapid (50kW to 149kW) and Ultra-rapid (150kW+) are unchanged.

Growth in rapid and ultra-rapid chargers

- At the end of April 2026, there were 28,089 rapid or ultra-rapid EV chargers (50kW+) across 6,902 locations.

- At the end of April 2026, there were 1,004 rapid charging hubs across the UK, defined as locations with at least eight rapid or ultra-rapid chargers, up 28% year-on-year.

Leading rapid and ultra-rapid charging networks at end of April 2026

- MFG EV Power: 2,866 chargers, 10.4% market share

- Osprey: 2,547 chargers, 9.3% market share

- BP Pulse: 2,491 chargers, 9.1% market share

Leading public EV charging providers

- Shell Recharge Ubitricity: 14,673

- Pod: 8,080

- Connected Kerb: 7,177

Areas with the most EV chargers at end of April 2026:

- Overall: Greater London (31,094), South East (15,555), Scotland (12,782)

- Rapid and ultra-rapid only: South East (3,942), Scotland (3,231), East of England (3,103)

Please note: From February 2026, Zapmap and the Department for Transport moved from counting devices to counting EV chargers as their primary metric. Figures from January 2026 and earlier use the previous device metric and are not directly comparable with 2026 figures.

How do EVs work?

How do EVs work?

EVs are powered by one or more electric motors rather than an ICE engine. These motors are powered by a rechargeable battery, which can be replenished by plugging the vehicle into an electric charger.

What factors affect EV performance?

Your real-world electric range may differ from the advertised figure (which often reflects a best-case scenario). Factors that affect EV performance include your driving style, weather conditions - and the degree to which features such as the in-car heating and air conditioning are used.

Smart energy recovery technology

EVs utilise technology that converts kinetic energy into electricity whilst braking or travelling uphill, automatically topping up the battery.

Glossary of EV terms

| Term | Definition |

|---|---|

| YoY | Year-on-year |

| Powertrain | The system responsible for generating a vehicle's power and transferring it to the road. |

| Market share | In the context of these guides, refers to the share of cars sold over a specified period, rather than share of the overall car parc. |

| EV | Electric vehicle |

| BEV | Battery electric vehicle |

| PHEV | Plug-in hybrid electric vehicle |

| HEV | Hybrid electric vehicle |

| MHEV | Mild hybrid electric vehicle |

| ICE | Internal combustion engine |

| ZEV | Zero emission vehicle |

| SMMT | Society of Motor Manufacturers and Traders |

| VED | Vehicle Excise Duty |

| ECS | Expensive Car Supplement |

| ZEV Mandate | A UK Government regulatory framework setting escalating annual targets for zero emission vehicle sales. The target for 2026 is 33% of new car registrations, rising to 80% by 2030. |

| Car parc | The total number of cars in use on UK roads at any given time. |