What is a Personal Contract Purchase?

Last updated May 21, 2021

If you’re thinking of buying a car, it isn’t just the make and model you need to think about. There are several financial considerations too, such as insurance costs, repair expenses and how you’re going to finance the vehicle. Understanding your finance options is therefore essential before signing on the dotted line.

This guide explains how to finance a car using a Personal Contract Purchase (PCP).

Value your car in under 30 seconds

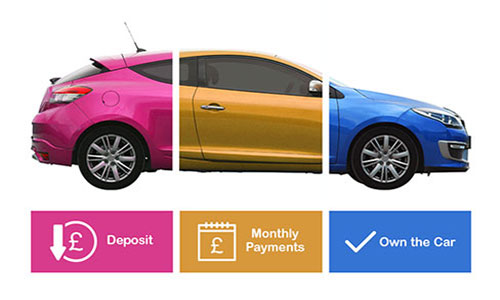

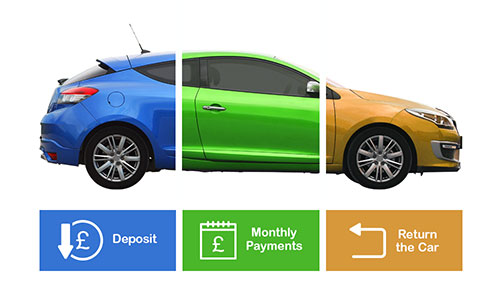

PCP explained

A Personal Contract Purchase is a popular finance option for purchasing new and used cars. You are essentially renting a car for the period specified in your contract, and at the end of the agreement you have the choice of:

- Returning the vehicle to the car finance company

- Assuming ownership of the car by paying the specified balloon payment

- Where the guaranteed minimum future value (GMFV) is lower than the market value of the car, you could use the equity in your current car towards a new car.

At the beginning of your application, you will need to pass a credit check, which considers your ability to meet the monthly payments. You must ensure the fees are affordable when taking out a PCP contract, as missed payments could lead to rising debt and have a negative effect on your credit score.

In most cases, PCP providers require a deposit of around 10% of the car’s purchase price. Some PCP agreements don’t require a deposit from the buyer, but these are rarer.

You should also consider the overall cost of the agreement and not just the monthly payments. For example, a finance company could be offering you a deal at £200 per month for 48 months with a small deposit, but the balloon payment could be unaffordable, meaning you won’t be able to purchase the car. Some dealerships offer 0% finance, but you should consider the whole offer as the finance company may recoup lost money elsewhere, such as the balloon payment, list price, or by not offering any discount.

Benefits of a personal contract purchase

-

There are no depreciation concerns as you can simply hand the vehicle back to the finance company at the end of the agreement

-

You can drive a car which may be otherwise unobtainable

-

Fixed monthly payments mean it is easier to manage your finances and budget for other expenses

-

Some dealerships offer extras such as maintenance packages, insurance and warranties, which allows for easier budgeting month-to-month.

-

You have several options at the end of the agreement.

Drawbacks of a personal contract purchase

-

The predicted minimum future value (PMFV) is likely to be set at an amount very close to the actual value of the car, so any positive equity you have in the car may be minimal

-

Your mileage will be limited, and you may incur a fee if you exceed the specified figure. If you have a change in circumstances which require you to travel more, this could get expensive

-

There are additional charges if you hand the vehicle back at the end of the agreement and there is any damage above ‘general wear and tear’

-

The car must have fully comprehensive insurance cover for the duration of the contract, which limits your options compared with if you owned the vehicle

-

You don’t own the car until you’ve made all the repayments

-

If you want to end the agreement early and the car is in negative equity, you’ll need to pay an early settlement fee.

What to do if you fall behind on monthly payments

Unforeseen circumstances and poor financial planning could result in missed monthly payments. To avoid such cases, consider your options carefully to prevent incurring further debt and affecting your credit rating.

Start by discussing your circumstances with your finance provider – they may offer you an early repayment option, enabling you to assume ownership of the car.

Alternatives to a PCP

A PCP isn’t the only option available when financing a car; several other options may better suit your needs:

-

Personal contract hire (PCH)

You will rent the car for a specified period, which is usually 24, 36 or 48 months. Unlike a PCP, you don’t have the option to purchase the car at the end of the contract and will need to hand the car back to the finance provider. The deposit and monthly costs are generally lower than the same car on a PCP and motorists have the option of adding a maintenance agreement that covers costs for servicing, glass damage, new tyres and annual car tax. A PCH is not suitable for motorists who want to own a car or change it midway through their contract. Regular long-distance driving is also unsuitable on a PCH contract.

-

Hire purchase (HP)

Similar to a personal loan, a HP requires you to make regular monthly payments and you own the car at the end of the agreed term, without a balloon payment. The main differences are that you don’t own the car until you have made all of the monthly repayments and you will have to pay a deposit at the beginning of the term. On the other hand, you are more likely to be accepted for a HP agreement than a personal loan due to less risk for the finance company. Advantages include returning the vehicle after 50% of the payments have been made and most dealerships will arrange the finance on your behalf.

-

Personal loan

A popular means of finance where you will have full ownership of a car. If you choose a personal loan, you will also become a cash buyer, which may help you negotiate a better deal. To get a loan with a low APR and limit your repayments, you will need to have a good credit rating. Unlike PCP, the car will be affected by depreciation, so you’ll owe more on the car than it’s worth. This isn’t the case with a PCP, as you don’t own the car until all repayments have been made.

-

Credit card

Providing there is a sufficient balance limit, you can use a credit card to buy a car. Suppose you have a good credit rating and get accepted for a 0% credit card; you could essentially buy a car interest-free, providing you pay off the balance within the promotional period.

If you choose to finance a car on a credit card, you will own the vehicle outright and you can always sell the car at any point to pay off the remaining balance; providing depreciation doesn’t exceed the outstanding balance.

However, dealerships may not accept credits cards as a valid payment method. It’s worth bearing in mind that credit cards are generally better suited to short-term borrowing and you’ll need to ensure you can pay off the balance relatively quickly to reduce the overall cost.