What is Personal Contract Hire (PCH)

Last updated May 07, 2021

Personal Contract Hire (PCH) is one of the most popular methods for leasing a car. PCH is a contract hire agreement available to individuals, whilst businesses can also arrange contract hire agreements for their workforce which excludes VAT.

Personal Contract Hire allows motorists to get a new car every few years (depending on the term of the agreement) with payments that are usually lower than getting the same car through Personal Contract Purchase, Hire Purchase, or a personal loan. If you are considering financing your car through Personal Contract Hire, it is essential you understand how it works, as well as the benefits and the drawbacks before entering into a financial agreement.

Value your car in under 30 seconds

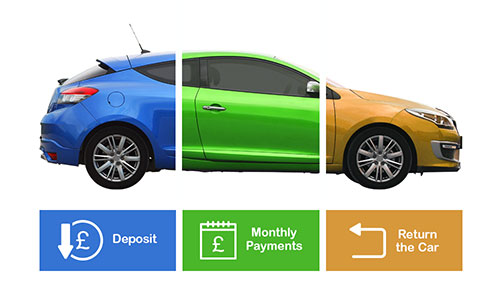

How does Personal Contract Hire work?

PCH is a long-term rental agreement where you pay a fixed monthly fee for the agreed period on your contract – most PCH deals are 24, 36 or 48 months. You will also be expected to pay a deposit for the vehicle, which is usually the equivalent of either 1, 3, 6, 9 or 12 months of your monthly payments. It’s worth noting that the higher the deposit, the lower the monthly payments.

Once you have found the vehicle you want to lease, you will be required to undergo a credit check, although the checks are usually less stringent than if you were taking out a PCP, HP, or personal loan to finance the car.

If you pass the credit check, the finance company will require you to pay the deposit. Some companies also charge a processing fee – once you make these payments, the leasing company will submit your order to the manufacturer for the car to be built.

When the car is ready, you can either collect it or arrange to have it delivered. You will be able to drive the car for the term of your agreement while adhering to the contract conditions, such as driving within the specified mileage. However, if you exceed your mileage allowance, you will incur additional fees when you return the car.

At the end of agreement you simply return the car to the finance company. Unlike PCP, there is no option to purchase the vehicle, although you may be able to extend your Personal Contract Hire agreement at the discretion of the leasing company. You will need to ensure that you return the car with all original documents and in good condition. If the vehicle has any damage deemed more than general wear and tear, you may be liable for the costs.

What's the difference between PCH and PCP?

Personal Contract Hire has several similarities and differences to Personal Contract Purchase. Like PCP, you will pay a deposit and fixed monthly payments which are set out in the contract, but the differences arise at the end of the agreement. With PCP, you can purchase the vehicle and become the legal owner, whereas with PCH there is no option to buy.

With both PCP and PCH, the finance company will legally own the vehicle for the contract’s duration, and you will be expected to make the monthly payments regularly. If you fail to do so, the car could be repossessed. The difference is that a car financed through PCH can be repossessed at any time without a court order, but a company offering PCP finance will require a court order once you’ve paid a third of the total amount payable.

As you pay for the depreciation of the vehicle through PCP, you generally pay more over the course of the agreement than a comparable car on Personal Contract Hire. Therefore, if you are one of the 4 in 5 people who return their vehicle at the end of their PCP agreement, it may be a better financial decision to opt for PCH.

Benefits of Personal Contact Hire

-

You can change your vehicle every 24 to 60 months depending on the term of your agreement

-

At the end of your PCH agreement you simply hand the vehicle over to the leasing company; therefore you are not affected by depreciation

-

You can drive a new vehicle that may otherwise be unobtainable without Personal Contract Hire

-

Monthly payments are generally lower than the equivalent vehicle on a PCP or HP agreement.

Drawbacks of Personal Contact Hire

-

All PCH agreements contain mileage restrictions – if you exceed this figure you will be expected to pay an agreed rate per mile

-

You will be liable for any damage to the vehicle that breaches the BVRLA ‘Fair Wear and Tear’ guidelines – this is chargeable when you return the car

-

It is difficult to terminate a Personal Contract Hire agreement early and if you choose to do so you will have to pay an early termination fee

-

You aren’t able to make any modifications to the car as you aren’t the legal owner

-

You need permission to take the car outside of the UK, and each time you want to do so there may be a charge.

What happens if I am unable to pay my monthly payments?

Unlike Hire Purchase where you can return the vehicle with no additional charges once you’ve paid half of the agreed payments, you cannot return a Personal Contract Hire vehicle early.

If you cannot make your monthly payments, it's worth speaking to your finance company as they may be able to assist with your financial situation. Early settlement figures, for instance, enable you to pay a percentage of your remaining monthly payments, which might be a better long-term financial decision.